By Dr Ray Johnson, Managing Director, Agricultural Appointments.

Australian agribusiness has been adversely affected by COVID-19, in particular those industry sectors exposed to decreased trade. Probably one of the worst sectors affected to date has been the premium seafood and aquaculture market such as premium specialty fish products (eg. Murray Cod) and Rock Lobster – nearly 100% of these products are sold into the Chinese market. But while March sales were devastated by COVID-19, the market rebounded quickly, especially due to the quick actions of the Australian Government on ensuring the logistics links were enhanced.

There have also been record livestock prices and reduced demand for Australian meat exports, which has heavily disrupted trade for meat processors. Crop production may also experience setbacks given the sector’s heavy reliance on imported crop protection equipment (i.e. fertilisers and pesticides). However, ABARE has predicted that while the pandemic precipitated a global economic downturn, it was unlikely to have a significant impact on demand for essential food products (An insight into Australian agricultural trade during the COVID-19 pandemic – and beyond, ABARE June 5th, 2020).

Our experience in dealing with agribusinesses nationally certainly concurs with the notion of significant disruption and uncertainty. We have seen many companies hold off on making key organisational appointments, in particular over the April-May period of 2020. But there has been renewed interest in moving forward as we moved into the June-July period. But the long-term implications of COVID-19 for Australian agriculture are at this time uncertain.

Richard Heath, the Executive Director of the Australian Farm Institute recently concluded:

“While the signs are positive that three months from now we will be able to report on some resolution of the immediate impacts of COVID-19, I am less optimistic that the long-term implications – and a thorough understanding of how Australian agriculture might have fundamentally changed as a result – will be as clear” (Farm Institute Insights, May-June, 2020).

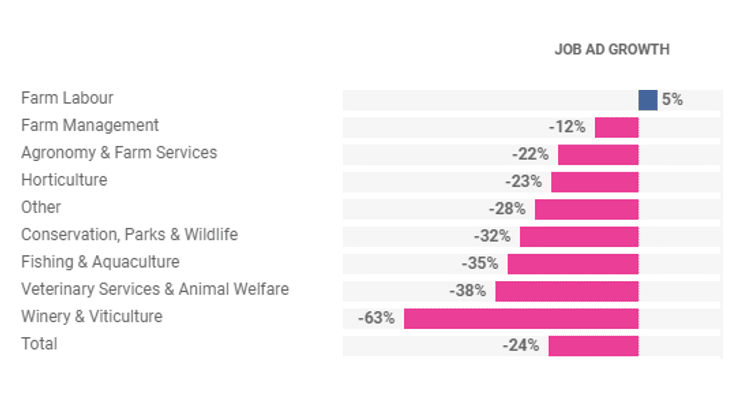

SEEK advertisements in the Farming sector suffered a 24% reduction in the two-month period from April 20 to June 20 compared with the same period last year, and this has resulted in a strong “levelling off” in employment from continual growth over the decade from 2010 to 2020. Indeed, the wine and viticulture sector recorded the largest single reduction in SEEK job ads of 63%, indicating that this sector was one of the most severely hit industries due to the COVID-19 pandemic, together with Fishing & Aquaculture.

The goal of Australian agriculture reaching its 2030 vision of $100 billion in production level will now probably not be achieved. The agriculture industry is well-known for its volatility and COVID-19 has added a new element to the significant risk profile of the sector. The full ramifications of the COVID-19 pandemic on Australian agriculture will not be fully known for some time, possibly 2-3 years. But there is significant optimism in the industry with increased rainfall in the eastern states and continued strong demand for food. The industry is adopting innovation and new technology at a rapid rate, meaning that agriculture will continue to strengthen as one of the key sectors for the future, despite COVID-19.

Figure 1. SEEK advertisements for the Farming, Animals & Conservation Sector for the period 2012 to end June 2020, relative to 2012 (Index 100=2012).Figure 2. SEEK advertisements for the Farming, Animals & Conservation Sector for the period April 2020 to end June 2020, compared with the same period in 2019.

Find out more about the outlook on the Australian and global agriculture industries post Covid-19, including an interesting report by Madeleine Swan, Associate Director of Agri Research Australia, ANZ.